HYBE Corporation Stock Price Prediction Using CNN-LSTM with CRISP-DM Framework

Article Sidebar

Main Article Content

Abstract

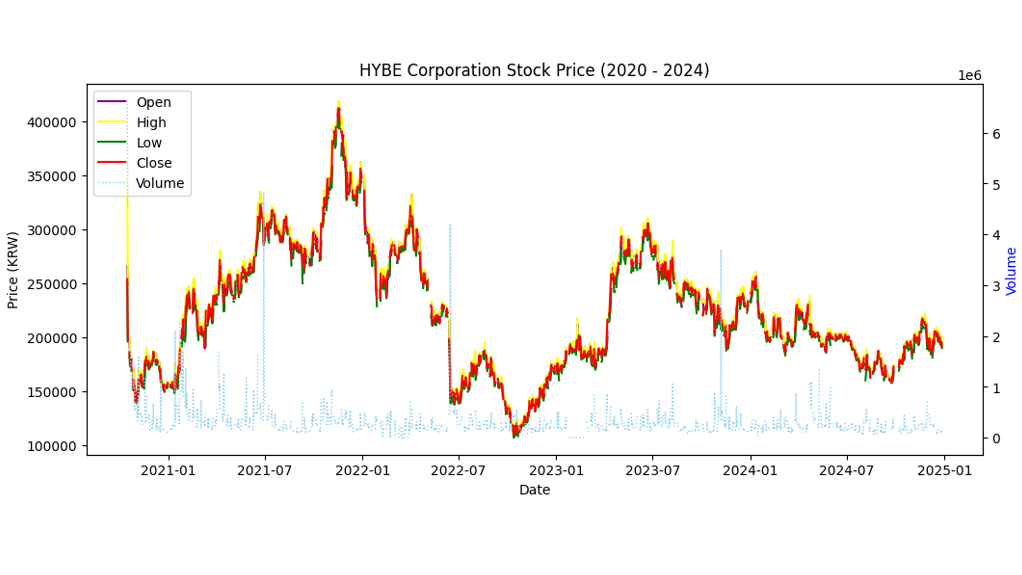

Digital transformation in financial analysis requires the application of computational models that can handle the complexity of the stock market efficiently and objectively. This study aims to predict the stock price of HYBE Corporation using the Convolutional Neural Network–Long Short-Term Memory (CNN-LSTM) model within the CRISP-DM (Cross Industry Standard Process for Data Mining) framework. The data used consists of daily stock prices of HYBE Corporation obtained from Yahoo Finance. The research process includes the main stages of CRISP-DM, namely business understanding, data understanding, data preparation, modeling, evaluation, and presentation of results. The CNN-LSTM model is designed to combine the ability of CNN to extract local patterns from time series with the advantage of LSTM in capturing long-term dependencies. To maximize the parameters used, this study also performed hyperparameter tuning using GridSearchCV on several key parameters. This process aimed to obtain the best combination of parameters capable of improving prediction accuracy and reducing the error value in the CNN-LSTM model. The evaluation results show that the CNN-LSTM model is capable of providing predictions with a very high level of accuracy. The Mean Squared Error (MSE) value is 0.00029, the Root Mean Squared Error (RMSE) is 0.01704, the Mean Absolute Error (MAE) is 0.01346, and the Mean Absolute Percentage Error (MAPE) is 2.15%. These low evaluation values demonstrate the model's effectiveness in handling stock market volatility while maintaining stability in predicting both short-term and long-term patterns.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.

References

Q. Zeng, Y. Tang, H. Yang, and X. Zhang, “Stock market volatility and economic policy uncertainty: New insight into a dynamic threshold mixed-frequency model,” Finance Res. Lett., vol. 59, p. 104714, Jan. 2024, doi: 10.1016/j.frl.2023.104714.

“World Bank Open Data,” World Bank Open Data. Accessed: Nov. 25, 2024. [Online]. Available: https://data.worldbank.org

J. Kim, K. Kim, B. Park, and H. Choi, “The Phenomenon and Development of K-Pop: The Relationship between Success Factors of K-Pop and the National Image, Social Network Service Citizenship Behavior, and Tourist Behavioral Intention,” Sustainability, vol. 14, no. 6, p. 3200, Jan. 2022, doi: 10.3390/su14063200.

H. Choi, “Do K-Pop Consumers’ Fandom Activities Affect Their Happiness, Listening Intention, and Loyalty?,” Behav. Sci., vol. 14, no. 12, p. 1136, Dec. 2024, doi: 10.3390/bs14121136.

F. Jin, S.-H. Kim, Y.-K. Choi, and B.-K. Yoo, “A Study on the Impact of Hallyu (Korean Wave) on Korea’s Consumer Goods Exports to China: Panel Analysis Using Big Data and Provincial-Level Data,” Sustainability, vol. 16, no. 10, p. 4083, Jan. 2024, doi: 10.3390/su16104083.

D. Yu and S.-Y. Choi, “Uncovering the Impact of Local and Global Interests in Artists on Stock Prices of K-Pop Entertainment Companies: A SHAP-XGBoost Analysis,” Axioms, vol. 12, no. 6, Art. no. 6, Jun. 2023, doi: 10.3390/axioms12060538.

C. Ji-won, “K-pop stocks struggle amid scandals, sluggish earnings.” Accessed: Jun. 19, 2025. [Online]. Available: https://asianews.network/k-pop-stocks-struggle-amid-scandals-sluggish-earnings/?

H. Wang, J. Wang, L. Cao, Y. Li, Q. Sun, and J. Wang, “A Stock Closing Price Prediction Model Based on CNN-BiSLSTM,” Complexity, vol. 2021, no. 1, p. 5360828, 2021, doi: 10.1155/2021/5360828.

A. H. A. Zili, D. Hendri, and S. A. A. Kharis, “Peramalan Harga Saham Dengan Model Hybrid Arima-Garch dan Metode Walk Forward,” J. Stat. dan Apl., vol. 6, no. 2, Art. no. 2, Dec. 2022, doi: 10.21009/JSA.06218.

M. Saberironaghi, J. Ren, and A. Saberironaghi, “Stock Market Prediction Using Machine Learning and Deep Learning Techniques: A Review,” AppliedMath, vol. 5, no. 3, p. 76, Sep. 2025, doi: 10.3390/appliedmath5030076.

W. Bao, Y. Cao, Y. Yang, H. Che, J. Huang, and S. Wen, “Data-driven stock forecasting models based on neural networks: A review,” Inf. Fusion, vol. 113, p. 102616, Jan. 2025, doi: 10.1016/j.inffus.2024.102616.

A. Sebastian and Dr. V. Tantia, “Multi-variate LSTM with attention mechanism for the Indian stock market,” Int. J. Inf. Manag. Data Insights, vol. 5, no. 2, p. 100350, Dec. 2025, doi: 10.1016/j.jjimei.2025.100350.

L. Alzubaidi, J. Zhang, A. J. Humaidi, A. Al-Dujaili, Y. Duan, O. Al-Shamma, J. Santamaria, M. A. Fadhel, M. Al-Amidie, and L. Farhan, “Review of deep learning: concepts, CNN architectures, challenges, applications, future directions,” J. Big Data, vol. 8, no. 1, p. 53, Mar. 2021, doi: 10.1186/s40537-021-00444-8.

H. Widiputra, A. Mailangkay, and E. Gautama, “Prediksi Indeks BEI dengan Ensemble Convolutional Neural Network dan Long Short-Term Memory,” J. RESTI Rekayasa Sist. dan Teknol. Inf., vol. 5, pp. 456–465, Jun. 2021, doi: 10.29207/resti.v5i3.3111.

C. O. Ewald and Y. Li, “The role of news sentiment in salmon price prediction using deep learning,” J. Commod. Mark., vol. 36, p. 100438, Dec. 2024, doi: 10.1016/j.jcomm.2024.100438.

J. Zhang and S. Li, “Air quality index forecast in Beijing based on CNN-LSTM multi-model,” Chemosphere, vol. 308, p. 136180, Dec. 2022, doi: 10.1016/j.chemosphere.2022.136180.

S. C. M. W. Tummers, A. Hommersom, C. Bolman, L. Lechner, and R. Bemelmans, “A new data science trajectory for analysing multiple studies: a case study in physical activity research,” MethodsX, vol. 14, p. 103104, Jun. 2025, doi: 10.1016/j.mex.2024.103104.

S. Panigrahi, Y. Karali, and H. S. Behera, “Normalize Time Series and Forecast using Evolutionary Neural Network,” Int. J. Eng. Res. Technol., vol. 2, no. 9, Sep. 2013, doi: 10.17577/IJERTV2IS90892.

J. Zhang, L. Ye, and Y. Lai, “Stock Price Prediction Using CNN-BiLSTM-Attention Model,” Mathematics, vol. 11, no. 9, p. 1985, Jan. 2023, doi: 10.3390/math11091985.

M.-C. Lee, J.-W. Chang, S.-C. Yeh, T.-L. Chia, J.-S. Liao, and X.-M. Chen, “Applying attention-based BiLSTM and technical indicators in the design and performance analysis of stock trading strategies,” Neural Comput. Appl., vol. 34, no. 16, pp. 13267–13279, Aug. 2022, doi: 10.1007/s00521-021-06828-4.

Y. Lecun, L. Bottou, Y. Bengio, and P. Haffner, “Gradient-based learning applied to document recognition,” Proc. IEEE, vol. 86, no. 11, pp. 2278–2324, Nov. 1998, doi: 10.1109/5.726791.

I. Irmawati, “Image Splicing Forgery Detection using Error Level Analysis and CNN,” Ultima InfoSys J. Ilmu Sist. Inf., vol. 14, pp. 79–86, Dec. 2023, doi: 10.31937/si.v14i2.3439.

I. D. Mienye and T. G. Swart, “A Comprehensive Review of Deep Learning: Architectures, Recent Advances, and Applications,” Information, vol. 15, no. 12, p. 755, Dec. 2024, doi: 10.3390/info15120755.

R. Raj and A. Kos, “An Extensive Study of Convolutional Neural Networks: Applications in Computer Vision for Improved Robotics Perceptions,” Sensors, vol. 25, no. 4, p. 1033, Jan. 2025, doi: 10.3390/s25041033.

W. Lu, J. Li, Y. Li, A. Sun, and J. Wang, “A CNN-LSTM-Based Model to Forecast Stock Prices,” Complexity, vol. 2020, no. 1, p. 6622927, 2020, doi: 10.1155/2020/6622927.

S. Hochreiter and J. Schmidhuber, “Long Short-Term Memory,” Neural Comput., vol. 9, no. 8, pp. 1735–1780, Nov. 1997, doi: 10.1162/neco.1997.9.8.1735.

B. Ghojogh and A. Ghodsi, “Recurrent Neural Networks and Long Short-Term Memory Networks: Tutorial and Survey,” Apr. 22, 2023, arXiv: arXiv:2304.11461. doi: 10.48550/arXiv.2304.11461.

P. Foroutan and S. Lahmiri, “Deep learning systems for forecasting the prices of crude oil and precious metals,” Financ. Innov., vol. 10, no. 1, p. 111, Jul. 2024, doi: 10.1186/s40854-024-00637-z.

H. Aldabagh, X. Zheng, and R. Mukkamala, “A Hybrid Deep Learning Approach for Crude Oil Price Prediction,” J. Risk Financ. Manag., vol. 16, no. 12, p. 503, Dec. 2023, doi: 10.3390/jrfm16120503.

C. P. F. Jr, “An Analysis of Time-Series Forecasting Models for Optimizing School-Based Feeding Programs,” J. Inf. Syst. Eng. Manag., vol. 10, no. 43s, pp. 1070–1075, May 2025, doi: 10.52783/jisem.v10i43s.8526.

K. Alkhatib, H. Khazaleh, H. A. Alkhazaleh, A. R. Alsoud, and L. Abualigah, “A New Stock Price Forecasting Method Using Active Deep Learning Approach,” J. Open Innov. Technol. Mark. Complex., vol. 8, no. 2, p. 96, Jun. 2022, doi: 10.3390/joitmc8020096.

B. Lim and S. Zohren, “Time-series forecasting with deep learning: a survey,” Philos. Trans. R. Soc. Math. Phys. Eng. Sci., vol. 379, no. 2194, p. 20200209, Feb. 2021, doi: 10.1098/rsta.2020.0209.

M. Veale, M. V. Kleek, and R. Binns, “Fairness and Accountability Design Needs for Algorithmic Support in High-Stakes Public Sector Decision-Making,” in Proceedings of the 2018 CHI Conference on Human Factors in Computing Systems, Apr. 2018, pp. 1–14. doi: 10.1145/3173574.3174014.

A. Adensamer, R. Gsenger, and L. D. Klausner, “‘Computer says no’: Algorithmic decision support and organisational responsibility,” J. Responsible Technol., vol. 7–8, p. 100014, Oct. 2021, doi: 10.1016/j.jrt.2021.100014.